📊Maximizing Wealth: AI-Driven Market Cycle Strategies

Wall Street Insider Book Project

Wall Street Insider Report

Expert Guidance in Wall Street. Join +1.5k Wall Street Insiders across 30 US states and 51 countries who are scaling 10x their investments Mastering the Market Cycles.

Maximizing Wealth: AI-Driven Market Cycle Strategies

Unlocking Investment Returns: The Role of Neural Networks and Signal-Based Models

Investment management has always been about decoding complex patterns and predicting market trends. Recent advancements in technology, particularly in artificial intelligence (AI), have opened up new possibilities for enhancing these predictions. By leveraging specific firm variables—or signals—investment professionals can anticipate future returns more accurately. This article delves into how neural networks utilize these signals to forecast financial returns, offering a clearer understanding of this cutting-edge technology.

The Foundation: Understanding Signals in Investment Management

Before diving into the complexities of neural networks, it's crucial to grasp the basic concept of signals within the realm of investment management. Signals are firm-specific variables that have shown potential in higher probabilities of higher future returns.

Alpha Hedge Algorithm Key Signals and Their Impact:

The Alpha Hedge Algorithm leverages a sophisticated understanding of market dynamics, distilled into key signals that guide investment decisions. Each of these signals not only provides insights into the market's current state but also significantly impacts the strategy's effectiveness and outcome.

Market Cycle: by analyzing the phases of market cycles, the algorithm adjusts its strategies to align with current stock market conditions. Recognizing whether the market is in an expansion, peak, contraction, or trough phase allows the algorithm to anticipate general market trends and position the portfolio to capitalize on these expected movements. The impact here is substantial as aligning investments with the market cycle can enhance returns and mitigate risks associated with market downturns.

Past Return Performance: It is a critical indicator used by the Alpha Hedge Algorithm to gauge the momentum of specific investments. Historical performance data serves as a reliable predictor of future returns, especially when contextualized with current market conditions. This signal allows the algorithm to identify trends and patterns in asset returns, enabling it to invest in securities that have demonstrated consistent performance over time. The strategic impact of this signal is its ability to leverage historical success as a proxy for future potential, thus optimizing the investment portfolio's growth trajectory.

Cycle Correlation: the Alpha Hedge Algorithm's strategy is its focus on selecting assets that exhibit low or no cycle correlation. This approach is integral for achieving true diversification, crucial in hedging against market volatility. By investing in non-correlated cycle assets, the algorithm can maintain portfolio stability even when stock markets fluctuate significantly. This strategic selection mitigates the risk of collective asset downturns and is especially valuable during market crises, ensuring that the portfolio is not wholly tied to the fortunes of the stock market.

Understanding these signals helps investors identify potentially profitable opportunities. However, the real magic happens when these signals are combined and analyzed through advanced models like neural networks.

Introduction to Neural Networks in Finance

Neural networks, a form of machine learning, mimic human brain operations to solve complex problems. In finance, they are used to process and analyze vast amounts of data, identifying patterns that are not immediately obvious to human analysts.

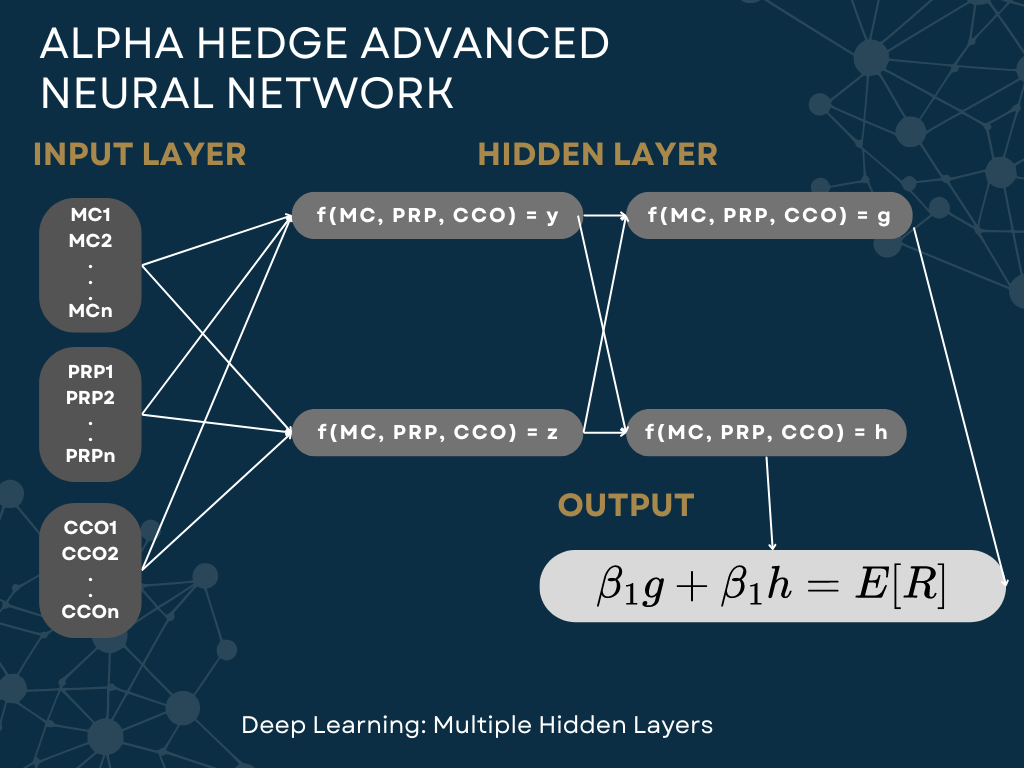

Simple Neural Network Setup:

To understand how neural networks operate, consider a basic example involving only 3 inputs: Market Cycle, Past Return Performance, Cycle Correlation. Here’s how a simple neural network might be structured to forecast returns:

Input Layer: Consists of the initial data points, such as Market Cycle (MC), Past Return Performance (PRP), Correlation, (CCO).

Hidden Layer: Processes the inputs using weighted sums and biases, essentially forming a linear combination of the inputs.

Output Layer: Produces the final prediction, the expected future returns of the assets.

This simplified setup helps illustrate the fundamental operations of a neural network, setting the stage for more complex applications.

Enhancing Portfolio Optimization Accuracy with Neural Networks

The power of neural networks in investment management lies in their ability to refine portfolio optimization through a process known as training. The network learns from historical data, adjusting its parameters to minimize errors between predicted and actual returns.

Training Process:

Forward Propagation: The network applies weights to the inputs to calculate returns.

Loss Function Evaluation: It calculates the returns using a loss function, typically the mean squared error.

Backpropagation: The network adjusts its weights to reduce the loss, improving the accuracy of returns over time.

By iteratively refining its portfolio optimization, a neural network can offer more precise forecasts than traditional models.

From Simple Regressions to Deep Learning

While initial neural network models may resemble simple regression analyses, they can evolve into more complex structures known as deep learning models. Deep learning involves multiple layers of neurons, each adding a layer of analysis and abstraction.

Advancing to Multiple Layers:

Multiple Hidden Layers: Each layer can learn different aspects of the data, from basic patterns to complex interactions.

Activation Functions: Functions like sigmoid or ReLU determine whether a neuron should be activated, introducing non-linear dynamics to the model.

These enhancements enable neural networks to handle complex, non-linear relationships in the data, which are often missed by simpler models.

Practical Implementation and Challenges

Implementing neural networks in investment management isn't without its challenges. It requires a robust dataset and careful tuning of parameters. Moreover, the choice of activation functions and the architecture of the network can significantly impact performance.

Steps in Implementation:

Training Sample: Used to fit the initial model.

Validation Sample: Helps fine-tune the model by testing its performance on unseen data.

Test Sample: Evaluates the final model’s performance to ensure it generalizes well to new data.

Common Challenges:

Overfitting: When a model is too closely fitted to the training data, it may fail to perform well on new, unseen data.

Computational Demands: Deep learning models, with their complex structures, require significant computational power.

Conclusion: The Future of Investment Management with AI

As neural networks become more sophisticated, their potential to revolutionize investment management grows.

These technologies allow for a deeper understanding of market dynamics, offering predictions that are not only accurate but also timely. While challenges remain, the integration of AI in financial analysis signals a shift towards more data-driven, objective investment strategies. The future of investment management looks promising, with neural networks leading the way towards more informed and effective decision-making processes.

Let's make this book a collaborative masterpiece!

So, can I rely on your support? Join me via Direct messages ↓

or Comments ↓