Maximizing Returns With Market Cycle Investing

Market Cycle Mastery Course: Lesson 2

Market Cycle Mastery: Lesson 2

Welcome back to our journey to Decoding the Market Cycles. I'm here to guide you further into the art and science of thriving in any market condition.

This approach enabled our clients to scale our investment portfolio by 10 times in the last decade.

In our last session, we unveiled the emotional drivers behind market cycles. Today, we take a pivotal step forward. You have recognized the challenges the market presents. Now, it's time to equip you with the statistical tools for maximizing returns.

The volatility of the market isn't just a barrier; it's a labyrinth. Navigating it requires more than just knowledge—it demands strategy. The Alpha Hedge strategy. Without it, you're at the mercy of the market's ebb and flow, caught in a cycle of reactive decisions.

But what if you could anticipate, with greater certainty, the market's movements? Not trying to predict, but proactively reacting through the market's phases. That's where our Alpha Hedge strategy comes into play, and where I, as your guide, provide you with a map and compass for this labyrinth.

The Alpha Hedge strategy is a beacon in the fog. It's a balanced approach, combining leveraged and protective assets to not just weather any market phase but to thrive. Today, we'll explore how to go a step ahead to identify the phase of the market cycle but how to optimize your Portfolio accordingly to maximize your returns.

Today we will focus on maximizing returns, but don’t worry, in the next lesson, you will learn how to minimize the risk.

In this lesson you will learn:

Maximizing Returns With Market Cycle Investing

Case Study: SPXL Direxion Daily S&P 500 Bull 3X Shares

In Which Phase of the Market Cycle Are We Now?

Get Started Now ↓

1. Maximizing Returns With Market Cycle Investing

1.1. Mastering the Alpha Hedge Strategy

The Alpha Hedge strategy algorithm observes three pieces of information and defines the portfolio optimization accordingly.

1.1.1. Alpha 1

Market Cycle phase. This you’ve already learned in Lesson 1 of this Course. With this analysis, we define at what time of the cycle the asset is.

1.1.2. Alpha 2

Past results don't guarantee future performance, but you shouldn't draft a quarterback for your team with low statistical performance. This doesn’t guarantee that he will perform well next season, external factors can interfere, but analyzing how this player acted in the past puts the probabilities on your side. That’s where the Alpha 2 indicator comes in.

Alpha 2 focuses on comparing the performance of entries and exits according to the Market Cycle in comparison to the Buy-and-Hold strategy.

If the cyclical performance outperforms the Buy-and-Hold strategy over the same period, it suggests a high probability for a long-term uptrends.

1.1.3. Alpha 3

Alpha 3 is about the Expectancy Ratio. Mathematical expectancy stands as a lighthouse, guiding ships safely to the shores of predictability and strategic success.

Often shrouded in the mist of mathematical complexity, this principle is indeed a cornerstone in not just financial forecasting but also in life decisions encompassing career planning and health management.

The Expectancy Ratio is a key component of our Alpha indicators, serving as a crucial element in the comprehensive framework of the Alpha Hedge Strategy.

The interpretation of Expectancy Ratio is the probability of profit per dollar risked.

1.1.4. Bottom Line

A favorable Expectancy Ratio (Alpha 3), combined with superior Alpha Hedge Performance over the Buy-and-Hold strategy (Alpha 2) during a Positive Cycle (Alpha 1), signals a green light for investments. The better the synergy of these metrics, the more suitable the asset is for your Portfolio.

2. Case Study: SPXL Direxion Daily S&P 500 Bull 3X Shares

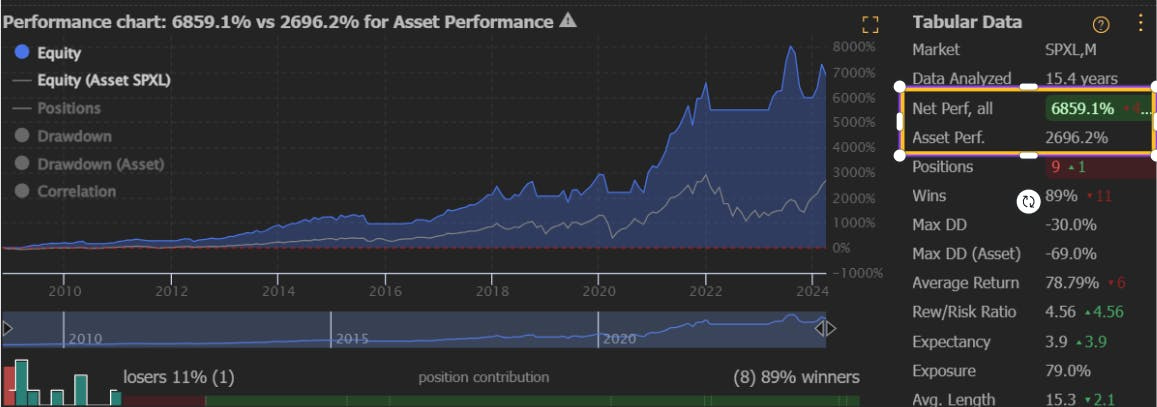

Consider the following example involving the Direxion Daily S&P 500 Bull 3X Shares SPXL ETF.

The first step is to identify the Alpha 1, Market Cycle Phase. By April 2024, the ETF is in Phase 3: Belief.

The next step is to calculate Alpha 2 and Alpha 3. For this, we configure the Alpha Hedge Algorithm on the Trendspider Platform.

As demonstrated in the image above, the Net Performance (performance of the Alpha Hedge Strategy) was 6,859.1%, surpassing the Buy-and-Hold strategy, which offered a 2,696.2% gain in15.4 years (without any new contributions or withdrawals, with profits reinvested and dividends excluded throughout the period).

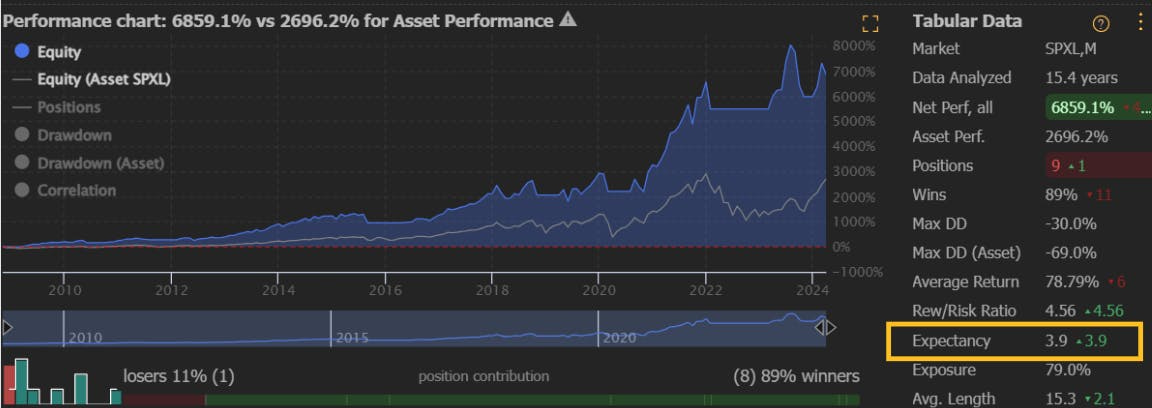

The Alpha 3 criterion is the Expectancy Ratio calculated for the SPXL ETF: 3.9 (Positive Expectancy).

2.1. Conclusion

A favorable Expectancy Ratio (3.9), combined with superior Alpha Hedge Performance over the Buy-and-Hold strategy (6,859.1% over 2,696%) during a Positive Cycle (Phase 3: Belief), signals a green light for investments in the SPXL ETF.

Tomorrow you will have access to the fundamentals of the Alpha Hedge Portfolio that lead our clients to overtake the Market over the last 11 years.

3. In Which Phase of the Market Cycle Are We Now?

With the Alpha Hedge Strategy, the fog clears. You move from uncertainty to a position of strength, anticipating market movements with confidence.

Remaining adrift in the volatility, vulnerable to every market whim doesn’t sound a smart alternative. But that's not your path. You're here to conquer, to achieve financial growth and stability.

Thank you for joining me today. In our next session, we'll dive into building a dynamic, diversified portfolio that embodies the principles of the Alpha Hedge strategy for Bonds, Currencies, Equity, Growth Stocks and Crypto and enables us to value our investment portfolio 10 times in the last decade.

Your journey to market mastery is just beginning. Together, we'll transform your financial future.

Thank you for taking this first step with me. Send your questions in the link below: