📊Data Evidence: Complex Models Outperform Simpler Ones

Decode the S&P 500 Market Cycle

Wall Street Insider Report

Decoding the S&P500 Market Cycle and sharing the backstage here in the Wall Street Insider Report.

Join +1.5k Wall Street Insiders across 30 US states and 51 countries.

Data Evidence: Complex Models Outperform Simpler Ones

More complex models can outperform simpler ones.

This evidence is crucial as it challenges the traditional econometric principle of parsimony, which favors simpler models.

The Ideal Data Length for Financial Machine Learning

Over-Parameterization and Overfitting

The concern with complex models is that they might overfit the training data, capturing noise rather than the underlying signal.

However, modern machine learning techniques, such as ridge regression and other regularization methods, can effectively control overfitting. By doing so, these techniques allow complex models to harness their full potential, improving out-of-sample prediction accuracy.

A primary focus is on high-dimensional linear prediction models, which are foundational in financial machine learning. These models often involve a large number of predictors and require sophisticated techniques to manage their complexity.

Pick My Brain: Best Tools for Analyzing Machine Learning Models

Ridge Regression with Generated Features

Ridge regression addresses over-parameterization by adding a penalty term to the regression model, which shrinks the coefficients of less important predictors.

This regularization helps mitigate overfitting, allowing the model to generalize better to new data.

Ridge regression can handle scenarios where the number of predictors exceeds the number of observations, a common situation in financial data.

Random Matrix Theory

This theory provides a mathematical framework for understanding the behavior of large covariance matrices, which are central to high-dimensional data analysis.

In the context of ridge regression, random matrix theory helps in predicting the performance of models as the ratio of predictors to observations increases. This theoretical underpinning is essential for evaluating the stability and reliability of complex models.

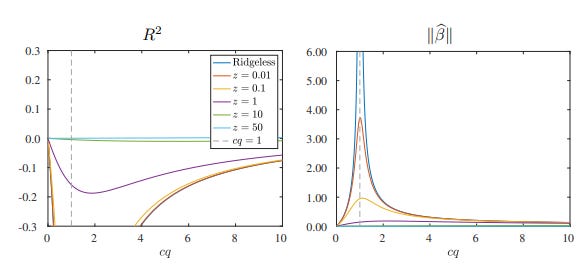

Figure 1: Expected Out-of-sample Prediction Accuracy From Mis-specified Models

Left Graph: R²

Vertical Axis (R²): Represents the expected out-of-sample prediction accuracy.

Horizontal Axis (cq): Represents the complexity of the model relative to the true model.

Lines and Colors: Each line represents a different value of the ridge shrinkage parameter z.

Interpretation:

Ridgeless Model (z → 0): The purple line represents the case with no ridge regularization (ridgeless regression). The R² initially decreases as model complexity increases but then starts to improve as the model becomes more complex.

Ridge Regularization: Other lines (e.g., z=0.01, z=0.1, z=1, z=10, z=50) show the effect of different levels of ridge regularization. For small values of z, the R² initially decreases, but as complexity increases, the regularized models perform better out-of-sample. Larger values of z (e.g., z=50) maintain a more stable R² across varying complexities.

Right Graph: ∥β^∥

Vertical Axis ∥β^∥: Represents the norm of the estimated coefficients, indicating the magnitude of the model parameters.

Horizontal Axis (cq): Represents the complexity of the model relative to the true model.

Lines and Colors: Each line represents a different value of the ridge shrinkage parameter z.

Interpretation:

Ridgeless Model (z → 0): The blue line indicates that without regularization, the norm of the estimated coefficients∥β^∥ becomes very large as the model complexity increases, peaking dramatically at cq=1, indicating overfitting.

Ridge Regularization: Other lines (e.g., z=0.01, z=0.1, z=1, z=10, z=50) show the effect of regularization. With regularization, the norm of the coefficients remains much more stable and lower in magnitude, even as the complexity increases, indicating better control over the overfitting problem.

There is Going to be a Rude Awakening for Lazy Investors

In financial contexts, where the data-generating processes are inherently complex and nonlinear, larger models can better capture these complexities.

As model complexity increases, out-of-sample prediction accuracy also improves.

This improvement occurs because complex models can approximate the true underlying structures of financial data more closely, even if they perfectly fit the training data.

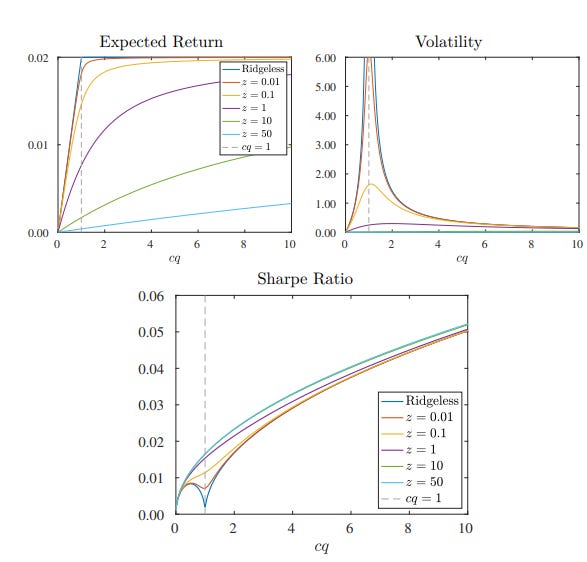

Top Left Graph: Expected Return

Vertical Axis (Expected Return): Represents the expected out-of-sample return of a trading strategy.

Horizontal Axis (cq): Represents the complexity of the model relative to the true model.

Lines and Colors: Each line represents a different value of the ridge shrinkage parameter z.

Interpretation:

Ridgeless Model (z → 0): The blue line shows the ridgeless model. As model complexity increases, the expected return initially increases rapidly and then plateaus.

Ridge Regularization: Other lines (e.g., z=0.01z = 0.01z=0.01, z=0.1z = 0.1z=0.1, z=1, z=10, z=50) show that models with some level of regularization can achieve higher expected returns more quickly as complexity increases. The highest returns are generally achieved when cq is between 2 and 4, depending on the level of z.

Top Right Graph: Volatility

Vertical Axis (Volatility): Represents the volatility of the trading strategy based on the model.

Horizontal Axis (cq): Represents the complexity of the model relative to the true model.

Lines and Colors: Each line represents a different value of the ridge shrinkage parameter z.

Interpretation:

Ridgeless Model (z → 0): The blue line indicates that without regularization, the model's volatility spikes dramatically at cq=1 and then decreases as complexity increases further.

Ridge Regularization: Other lines (e.g., z=0.01z = 0.01z=0.01, z=0.1z = 0.1z=0.1, z=1, z=10, z=50) show that regularization helps maintain lower volatility, especially around the critical cq=1 point. This stabilization is more pronounced with higher values of z.

Bottom Graph: Sharpe Ratio

Vertical Axis (Sharpe Ratio): Represents the risk-adjusted return of the trading strategy, combining expected return and volatility.

Horizontal Axis (cq): Represents the complexity of the model relative to the true model.

Lines and Colors: Each line represents a different value of the ridge shrinkage parameter z.

Interpretation:

Ridgeless Model (z → 0): The blue line shows a dip around cq=1cq = 1cq=1, indicating poor performance due to high volatility. However, the Sharpe Ratio improves as cqcqcq increases further.

Ridge Regularization: Other lines (e.g., z=0.01z = 0.01z=0.01, z=0.1z = 0.1z=0.1, z=1, z=10, z=50) indicate that regularization generally leads to a higher and more stable Sharpe Ratio. The highest Sharpe Ratios are achieved with intermediate levels of complexity, particularly when cq is between 2 and 6, depending on the level of z.

References

Kelly, B., & Xiu, D. (2023). Financial Machine Learning. SSRN.

Portfolio Review: 06/17/2024

The Alpha Hedge Portfolio experienced a significant upward movement on Monday, aligning with broader market trends as US stocks surged to new all-time highs. The S&P 500 SPY 0.00%↑ recorded its 30th record close of the year, contributing to a daily performance increase of +1.7% for the portfolio.

This positive momentum is also reflected in the portfolio's monthly performance, which stands at +7.6%, underscoring the portfolio's strong positioning and effective strategy amid current market conditions.

Over the past decade, our subscribers have outperformed the American Market Decoding the S&P 500 Market Cycle.

You too can make investment decisions based on objective data.

That's where the Wall Street Insider Report comes in. We've developed a unique approach to investment management that puts you back in the driver's seat.

Know more about our 5-Year Plan and join +1.5K Pro Investors and Finance Professionals across 51 countries who are exponentially growing their - and their clients - wealth for over a decade.↓